Institutional-Grade

Portfolio Software.

Completely Free.

Not just another finance site — a full portfolio construction platform in your browser. Five optimization methods, twenty-seven asset classes, Monte Carlo simulation, backtesting. Sign up with an email and everything unlocks.

Full access with just an email · No credit card · Runs privately in your browser

Three Workflows

Optimize. Simulate. Retire.

One platform for the full lifecycle of portfolio construction.

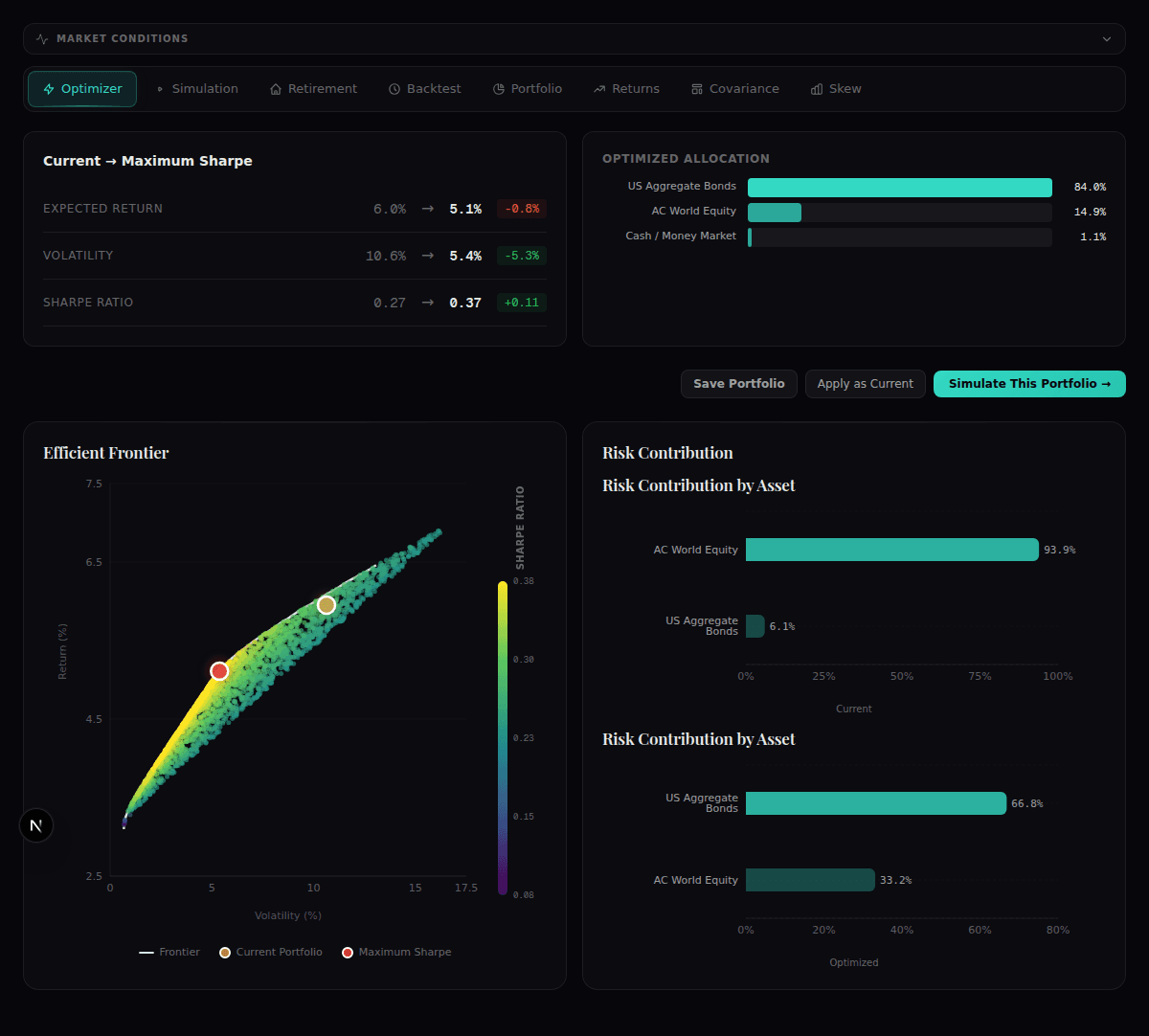

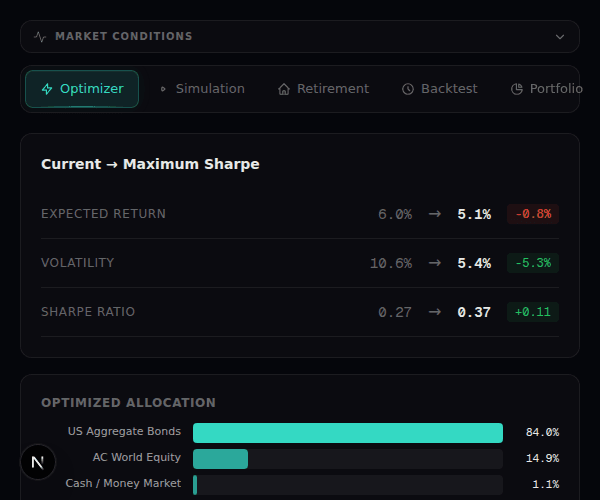

Optimize

Max Sharpe, Min Variance, Risk Parity, HRP, Black-Litterman. See exactly how your portfolio changes with delta arrows and what-changed tables.

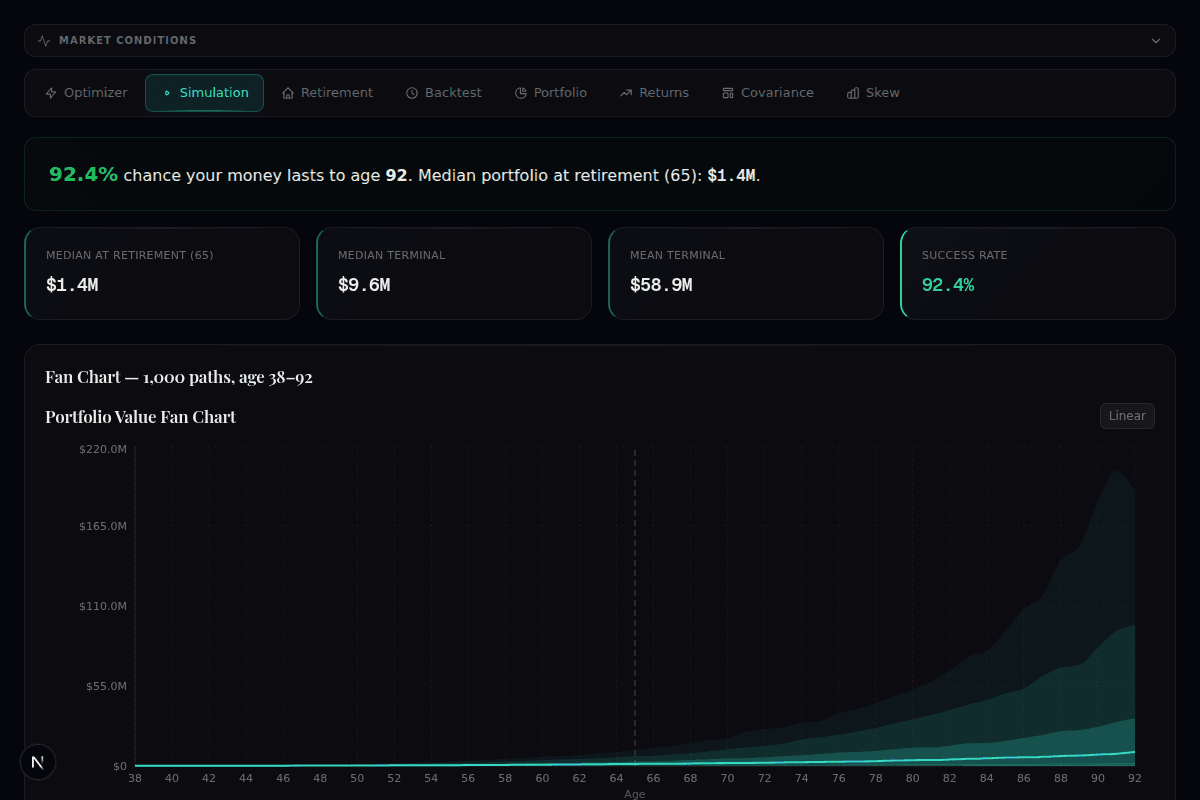

Simulate

1,000 Monte Carlo paths with fan charts, guardrails spending, and full risk metrics. See your probability of success at every withdrawal rate.

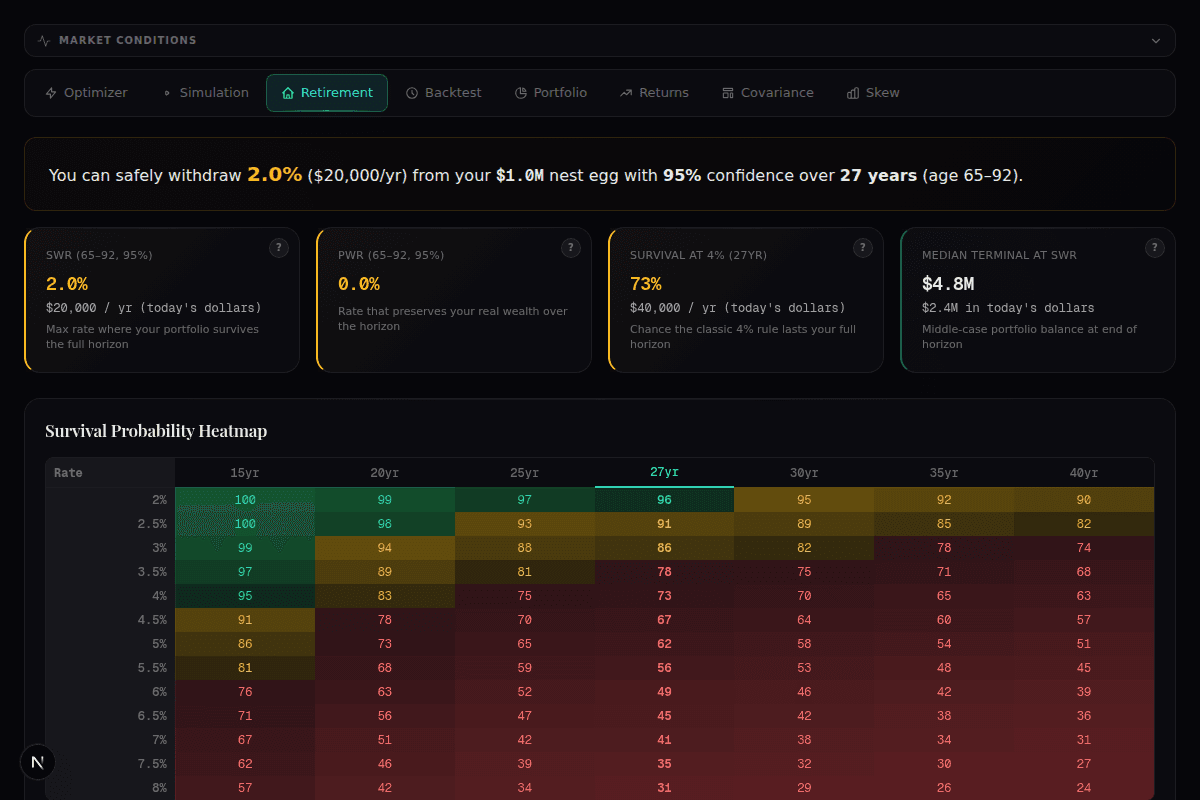

Retire

Safe withdrawal rate analysis with survival heatmaps across 13 rates and 7 horizons. Click any cell for a detailed fan chart.

The Difference

Why forward-looking data changes the answer

Almost every free portfolio tool optimizes on the past — it feeds in historical returns and finds the mix that would have worked. The trouble is that the last four decades were shaped by falling interest rates and expanding valuations, conditions unlikely to repeat. Optimize on that history and you build a portfolio for a world that has already happened.

Portfolio Lab runs on J.P. Morgan's 2026 Long-Term Capital Market Assumptions — the same forward-looking return, risk, and correlation estimates used by pension funds and endowments managing trillions. They reflect where valuations and yields actually are today, not where they have been. That single change moves the efficient frontier, the safe withdrawal rate, and the optimal Bitcoin weight, often substantially.

And everything runs in your browser. No account is required for the free tools, and no portfolio data is ever sent to a server. You get the institutional method and the institutional data — without the institutional price tag or the privacy trade-off.

Live Data

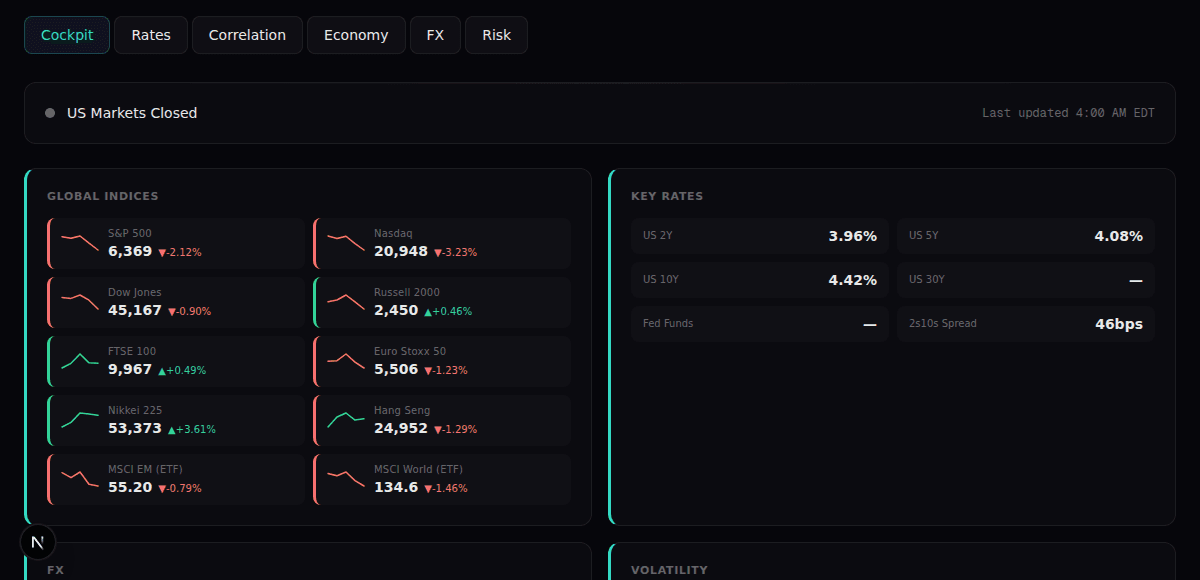

Global Macro Cockpit

Real-time indices, yield curves, credit spreads, CAPE valuations, factor performance, and FX — all in one view.

Try Before You Sign Up

14 Free Tools

Every tool below runs right now, no account needed. When you want the full platform — all 27 asset classes, every optimization method, saved portfolios, PDF reports — a free account is one email away.

Reference Allocations

Model Portfolios

Forward-looking expected returns, volatility, and Sharpe ratios for the most-cited portfolio strategies — each shown with optional Bitcoin variants.

Research & Insights

Latest Analysis

Built for Anyone Who

Takes Investing Seriously

Whether you manage other people's money or just your own.

Independent Advisors→

Institutional-grade tools without the Bloomberg terminal price tag. White-label PDF reports for clients.

Self-Directed Investors→

Stop guessing allocations. Build portfolios backed by J.P. Morgan's forward-looking data.

FIRE Planners→

Monte Carlo simulations, safe withdrawal rates, and retirement survival analysis with real assumptions.

Finance Students & CFA Candidates→

See portfolio theory in action. Efficient frontiers, risk parity, and factor models with real data.

More Resources

See It In Action

5-Minute Walkthrough

Watch how to go from zero to optimized portfolio in minutes.

Pricing

Free. No Catch.

One plan. Everything included. No credit card required.

- 27 asset classes with JPM 2026 data

- 5 optimization methods incl. Black-Litterman

- Monte Carlo simulation with fan charts

- Retirement analysis with survival heatmaps

- Historical backtesting (2002–2025)

- Live market dashboard with CAPE valuations

- Bitcoin & custom ticker support

- PDF reports & unlimited saved portfolios

- Multi-currency (USD, GBP, EUR, AUD, CAD, JPY)

Sign up with an email and the whole platform unlocks. That's it.

Questions

Frequently asked questions

Is Portfolio Lab really free?

Yes. Portfolio Lab is free software, not a free trial. The public tools work with no account at all, and a free account — just an email, no credit card — unlocks the full platform: the complete 27-asset optimizer with all five methods, Monte Carlo simulation, retirement analysis, unlimited saved portfolios, and PDF reports. There is no paid tier waiting to upsell you.

Is Portfolio Lab a website or software?

It works like software — a full portfolio construction application that happens to run in your browser. There is nothing to install and nothing to update. Sign up free with an email and you get the complete optimizer, simulation, and reporting suite, with every calculation running privately on your own device.

What optimization methods does it use?

Five: Maximum Sharpe, Minimum Variance, Risk Parity, Black-Litterman with custom views, and Hierarchical Risk Parity, applied across 27 asset classes. These are the same methods used by institutional multi-asset teams.

What data are the numbers based on?

J.P. Morgan's 2026 Long-Term Capital Market Assumptions — forward-looking return, risk, and correlation estimates rather than historical averages. You can also compare the assumptions of five major research firms side by side.

Do I need a finance background?

No. Each tool explains what it does in plain language and handles the math for you. When you want the detail, the full methodology documents every formula and data source.

Is my portfolio data private?

Yes. Every calculation runs in your browser. Your holdings, allocations, and projections never leave your device and are never sent to a server.

Can I analyze Bitcoin in a portfolio?

Yes. Bitcoin is a first-class asset with its own forward-looking assumptions, so you can size it with mean-variance optimization, backtest it inside a 60/40, and stress-test it in retirement — not just guess.

Start Building Better Portfolios

One email gets you the full platform — optimizer, simulations, retirement analysis, and PDF reports. Free, with no credit card.

Create Free Account